AoCass Information Systems says April freight markets have finally cooled. Cass, a payments management service, reported last month that a freight recession is likely. Inflation, notably rising diesel prices, interest rate hikes, and a shift in consumer buying habits to services have prompted the fall and may be the impetus for further freight industry down turning. The freight industry is also a good anecdote, and perhaps a microcosm of a larger scale economic recession that indicators suggest may already be upon us.

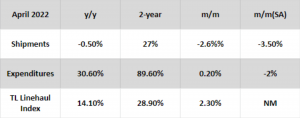

April freight shipments were down 0.5% year-over-year and 3.5% from March (seasonally adjusted). The research warned that “further softness is on the horizon” as comps get harder and the ripple effect of China’s production shutdowns throughout the Spring are felt. With container ship backlogs off North American ports, the direct consequences on completed goods imports are likely throughout June & July.

Small spot market carriers will feel the decline harder. Last year, many drivers got permission to operate on their own and bought expensive equipment to seek high spot rates. The increased capacity and falling freight demand have impacted spot market fundamentals, making it tougher for small load board operators.

Small spot market carriers will feel the decline harder. Last year, many drivers got permission to operate on their own and bought expensive equipment to seek high spot rates. The increased capacity and falling freight demand have impacted spot market fundamentals, making it tougher for small load board operators.

SCass’ expenditures subindex increased 0.2% sequentially from a March record. Seasonally adjusted, the dataset dropped 2%. Shipments fell, lowering the month-over-month change. Shippers aren’t relieved by the flat month. The expenditures index was 30.6% higher than a year earlier and 90% above pandemic levels (April 2020). The index rose 38% last year and is expected to rise 24% in 2022 if seasonal trends hold.

Inferred rates (expenses/shipments) rose 31.3% year-over-year and 1.5% from March. Fuel surcharges are boosting the dataset’s new high. The research predicted substantial slowing in the following six months.

Tim Denoyer, vice president and senior analyst at ACT Research, a leader in market data, industry analysis, and forecasting for the commercial vehicle and transportation markets, remarked, “2022 saw a huge improvement in driver availability and a slowdown in freight demand.” This deflationary combination will take months to filter through contract rates. New COVID versions or a worsening chip scarcity could reduce Class 8 truck output, he said.

Table: (SONAR: NTIL.USA, VCRPM1.USA). National Truckload Index (linehaul only – NTIL) is based on 250,000 lanes and 10,000 daily spot market transactions. NTIL is a seven-day average of linehaul spot fares excluding fuel. The green line shows the seven-day per-mile average dry van contract load rate without gasoline (reported on a 14-day lag). FreightWaves SONAR information is here.

Excess miles and accessorial fees also boost assumed rates. Rail congestion has forced intermodal freight onto trucks. Modal shift-related expenditures and distances inflate the index. Denoyer feels the genuine freight cost is between the inferred rate dataset (+31%) and the truckload linehaul index (+14.1%). April’s linehaul index rose 2.3% from March.

Normal contract scheduling suggests [the TL linehaul] index can rise a bit longer after the high in spot prices, but the clock is ticking, said Denoyer. “While this is excellent news for some, particularly shippers and those worried about inflation, fleets should prepare.” Far from stagflation, these patterns imply freight rate deflation.