Thanks to Matt Hertz for this share, featured in the August 1st edition of Sent Items. This tweet is featured in the intro (talk about hooking the reader in). If you’re not reading Matt already, we highly recommend.

Thanks to Matt Hertz for this share, featured in the August 1st edition of Sent Items. This tweet is featured in the intro (talk about hooking the reader in). If you’re not reading Matt already, we highly recommend.

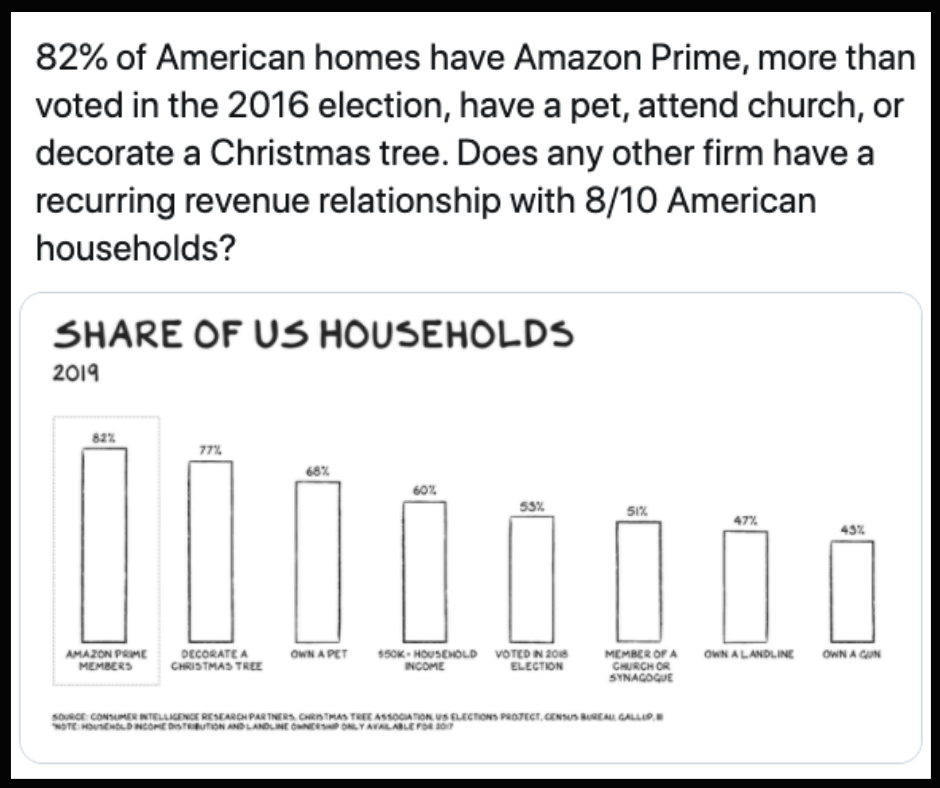

Data sets like this – those that come stock with a few points of comparison – are our favorite kind.

That said, they can sometimes be both parts amazing and frightening.

Amazing… that it is possible for a company to create this type of relationship with so much of the country. At Fosdick, we talk alot about client relationships through the lens of our many subscription box and continuity business clients.

Love them or hate them, it takes a high level of service for Amazon to achieve and maintain numbers like this. Reverse engineering that service could be a great way for founders of eCom and sub-box brands to think through many related challenges.

When we say service and customer relations, we are speaking in the most general sense. It is more than likely that for smaller brands these will be vastly different from the largest e-tailer in the world. Amazon’s game is convenience. Consumers will always pay for convenience. They leverage this with affordability of Amazon branded and owned products.

That is the X-factor for the eCommerce giant. Start-ups will likely struggle to carve out their own path as an DTC company following this exact model. Or perhaps it just means a mindset shift in what convenience and affordability mean in the context of the value small brands provide consumers.

Curated style boxes are convenient for those that dislike the clothes shopping experience. Continuity consumables are convenient for those who don’t want to worry about reordering each month. A higher quality, niche consumable can easily sell itself as the affordable option for a specific demographic. Take LOLA for instance – a client partner to Fosdick offering continuity, organic feminine care products. LOLA’s customers place a great deal of importance on the quality of the products they use. They want organic products, and it is a genuine convenience for those products to show up on their doorstep as per the schedule they have set. The price LOLA customers pay for that convenience is a great value!

Frightening…that there are 20% more prime memberships (which is by no means a cheap subscription) than there are $150k annual household incomes and 27% more people pay the $119 a year than bothered to vote in 2018 (55% – which actually seems high based on the voting statistics we tend to see in the news).

The Takeaway

Most consumers see an easy shopping experience as one worth the price of admission. This therefore makes that experience an affordable one, regardless of the actual monetary cost (and assuming consumers have allocated a relatively flexible budget such that they are in a position to explore various product options).

And despite this, and no matter how many negative stories feature Bezos and company, the numbers of Amazon users (and now premium users) keep growing. There are a few reasons why this might be:

- For many product categories, there are still limited DTC options.

- So many companies providing great customer relations and highly specific products within their respective categories are also selling Amazon.

- If a start-up is not selling on Amazon, the e-tailer has reproduced the small brand’s product line in one form or another.

Perhaps this is the tip of the bell curve for the retailer. As mobile first shopping continues to grow with players like Instagram getting involved, and as companies like Walmart build out their own subscription models (all of which can be optimized for convenience and safety by emerging fintech and digital payment services), the playing field will start to level off. Or perhaps, Amazon always intended to eventually lean on its other, more infrastructural business channels. Time will tell…